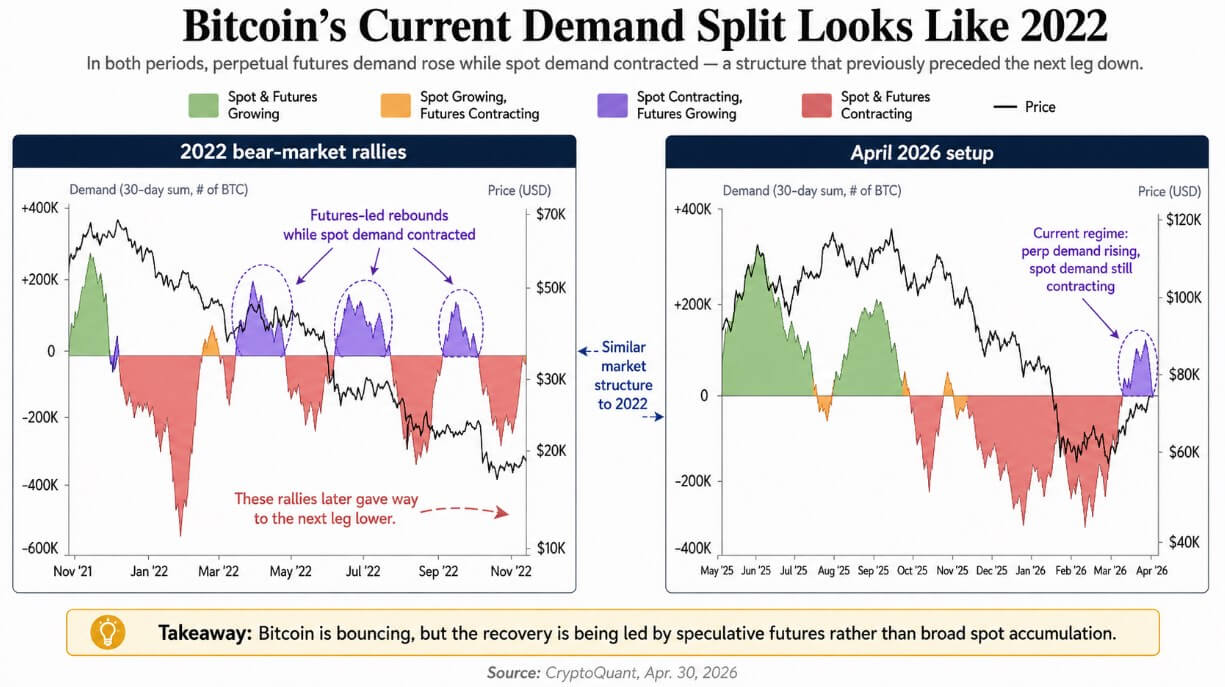

CryptoQuant’s newest knowledge from April 30 exhibits that perpetual futures are driving Bitcoin’s restoration whereas spot demand continues to be contracting. This is identical market construction seen in the course of the 2022 bear market rebound, the place a leverage-driven rally gave option to new draw back.

Spot purchases by means of exchanges, ETFs, or direct on-chain accumulation characterize dedicated capital. On the similar time, perpetual futures enable merchants to take directional publicity utilizing borrowed capital, typically at multiples of the collateral, with out holding the underlying asset.

When each types of demand develop concurrently, the rise tends to be self-reinforcing. If futures lead and there’s a spot lag, leveraged merchants will be capable of fund the rebound and face a pressured exit if the value strikes towards the futures.

2022 comparability

A number of bear market rallies in 2022 have seen the identical sample, with perpetual futures demand recovering earlier than spot demand recovered. Costs rallied and leveraged positions have been stripped out as spot patrons proved too skinny to soak up the promoting.

The bounces gave the impression to be constructive, however every resolved into the following leg.

In accordance with CryptoQuant’s chart, Bitcoin will return to its present regime in April 2026, the place spot contracts are shrinking and futures contracts are increasing. Equally, borrowed capital is re-emerging earlier than actual money demand emerges, which is strictly the situation that made the failed 2022 rally so fragile.

The dimensions of at this time’s futures markets makes their vulnerability a much bigger variable. In accordance with CoinGlass knowledge, the 24-hour Bitcoin futures buying and selling quantity was $47.64 billion, in comparison with spot buying and selling quantity of $4.07 billion, a ratio of roughly 11.7 instances, and open curiosity as of April thirtieth was roughly $54.19 billion.

Perpetual futures can contain borrowed capital of as much as 50 instances the collateral on some platforms, so comparatively small value actions can set off large-scale liquidations.

The depth of the market is quickly examined as spot quantity reaches $4 billion per day and long-side flushes start.

What ETF knowledge provides

The movement of US spot Bitcoin ETFs has not too long ago raised alarm over the market construction, with knowledge from Pharcyde Buyers displaying cumulative outflows of $490.5 million from April 27 to April 29.

The long-term ETF image is holding its form, however the ETF’s bid value has turn out to be risky on the actual second that futures positions are increasing.

| metric | present studying | why is it necessary |

|---|---|---|

| BTC futures quantity, 24 hours | $47.6 billion | Derivatives exercise dominates the market |

| BTC spot quantity, 24 hours | $4.07 billion | Spot assist is far smaller than futures buying and selling |

| Futures/Money Quantity Ratio | 11.7 instances | Reveals that the rally is considerably leverage-driven |

| BTC open curiosity | $541.9 billion | Giant leverage place base that may be unwound |

| US Spot BTC ETF Flows, April 27-29 | -$490.5 million | ETF demand has been unstable not too long ago. |

| IBIT cumulative web influx | ~$65.2 billion | Lengthy-term institutional investor demand stays sturdy |

| Whole cumulative inflows of US spot BTC ETF | ~$58.1 billion | Structural ETF bidding stays general optimistic |

IBIT alone accounted for roughly $65.2 billion in cumulative web inflows, bringing the whole for your complete U.S. Spot Bitcoin ETF class to roughly $58.1 billion, a quantity that displays true structural shopping for that won’t be current in 2022.

From April 13 to April 29, IBIT nonetheless absorbed web inflows of roughly $1.47 billion, sustaining long-term institutional circumstances. The short-term view is that ETF bids presently don’t present clear value assist at a time when futures positioning is most wanted.

bull incident

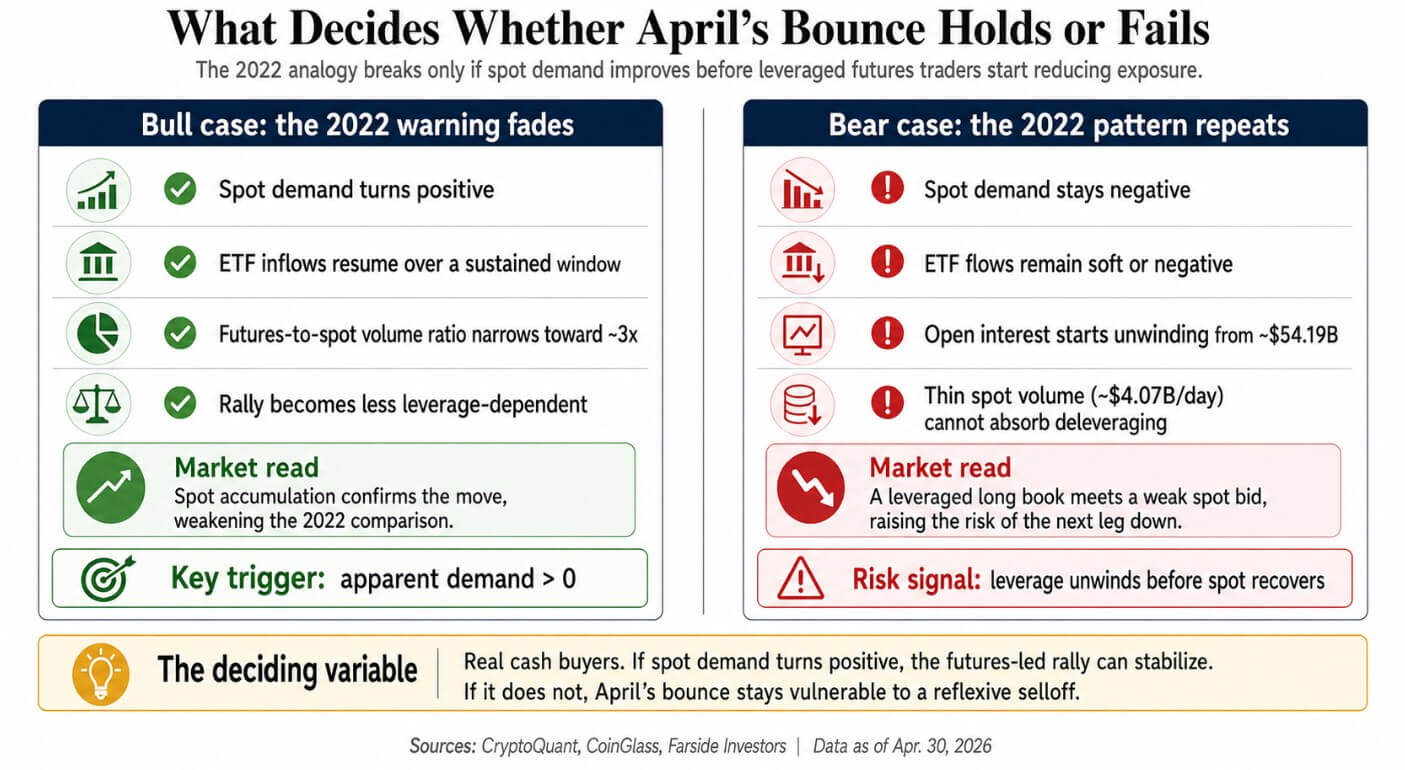

The 2022 analogy breaks down when spot demand turns optimistic earlier than leveraged merchants begin decreasing their publicity. A transfer in CryptoQuant’s obvious demand metric above zero is the cleanest invalidation set off that spot accumulation confirms a futures-driven transfer.

The structural hole between 2026 and 2022 additionally offers foundation for the bullish case. Bitcoin now regulates spot ETFs within the US, deeper institutional infrastructure, and sustained company monetary bidding that did not exist 4 years in the past.

CryptoQuant’s April 1 memo, which warned of a big contraction in spot demand, additionally acknowledged that ETF and company shopping for was accelerating.

A bullish case is executed by patrons scaling up quick sufficient to convey spot demand again into optimistic territory. If ETF inflows resume for a sustained time period and the futures-to-spot quantity ratio narrows towards 3x the general market, the market construction argument will itself weaken.

bear incident

In a bearish case, solely leveraged merchants ought to scale back their publicity earlier than spot demand turns optimistic. All that’s required is for leveraged merchants to begin decreasing their publicity earlier than spot demand turns into optimistic.

With open curiosity reaching $54 billion, even a partial unwind would end in a big absolute selloff, and with spot buying and selling quantity of roughly $4 billion per day, the market doesn’t have the depth to soak up a speedy unwind with out vital value declines.

This reflexivity additional exacerbates the danger, as falling costs drive leveraged longs in the direction of liquidations, liquidations drive costs down, and the cycle mechanically progresses till spot demand is deep sufficient to keep up the ground.

The bear market ends when demand for each spot and futures recovers.

With the present setup, futures are recovering on their very own, and if these circumstances maintain, Bitcoin may have recreated the demand construction of the failed 2022 rally. The tone of obvious on-chain demand and ETF flows within the coming weeks will decide whether or not the April rebound joins or leaves that record.

Both bodily patrons step in and validate futures-driven strikes, or the market learns what a leveraged lengthy guide seems like when spot bids are too skinny to maintain the ground.