The Ethereum Basis (EF) introduced on April eighth that it’s going to convert 5,000 ETH right into a stablecoin by means of CoWSwap’s TWAP function to fund analysis, grants, and donations.

This announcement reignited the controversy over the aim of the Basis’s monetary overhaul. Final 12 months, EF moved its monetary property to DeFi, borrowed utilizing ETH as collateral, after which started a staking initiative centered on round 70,000 ETH.

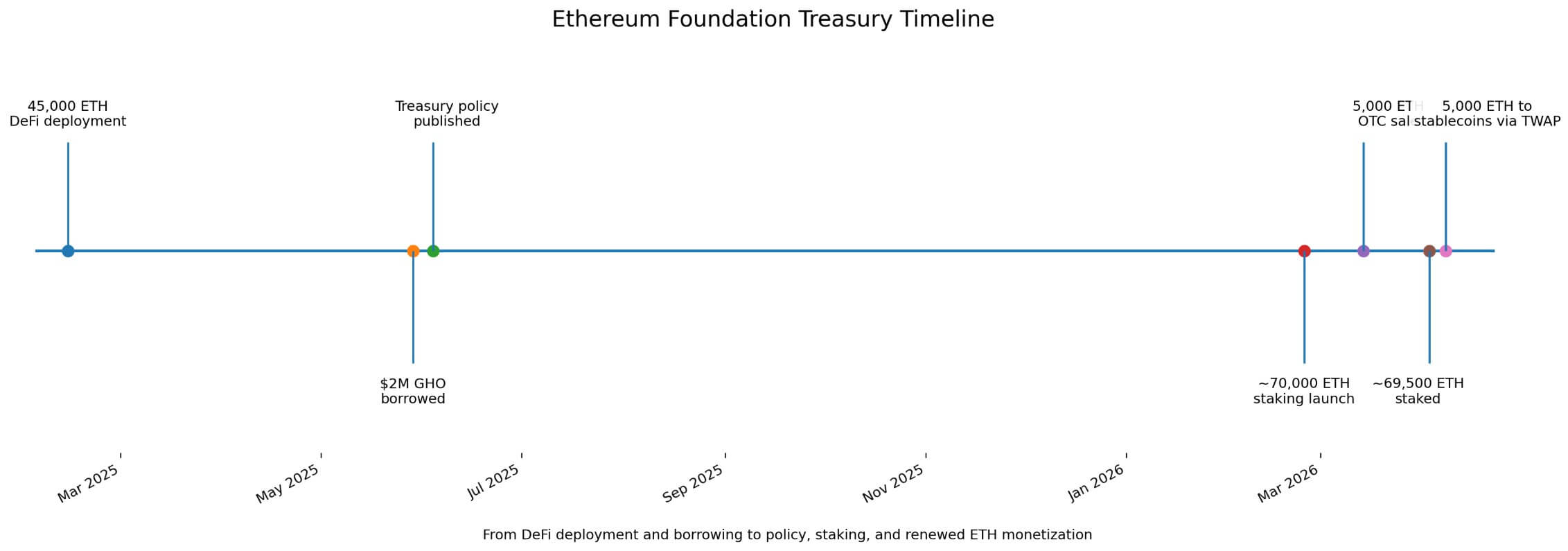

The truth outlined within the EF’s June 2025 monetary coverage suggests a distinct mannequin. It tied monetization to a fiat-denominated operational buffer, retaining ETH gross sales, staking, and stablecoin borrowing inside the identical Treasury framework.

On February 13, 2025, the EF Treasury introduced that it had deployed 45,000 ETH throughout Spark, Aave Prime, Aave Core, and Compound. On Might 29, the corporate borrowed $2 million in GHO for its Aave place.

This transfer had symbolic weight because it confirmed that EF was utilizing DeFi rails to lift working capital with out promoting spot ETH.

By early April, that interpretation had permeated the retail dialog, with a Reddit put up claiming that EF was “now not promoting.” One commenter replied, “I am glad they stopped promoting it.”

Regardless of the anecdotal proof, this type of chatter reveals how a stronger model of the paper was already in circulation earlier than EF introduced its April 8 change.

Gross sales are ongoing

EF launched its staking initiative on February twenty fourth, asserting that it could stake 70,000 ETH and the rewards could be returned to the Treasury.

On March 14th, we accomplished a 5,000 ETH OTC sale to BitMine at a median worth of $2,042.96. On April third, on-chain exercise introduced the entire quantity of staking to roughly 69,500 ETH, transferring us nearer to our objective. Then got here the CoWSwap transformation on April eighth, highlighting that promoting and staking have already been working in parallel for a number of weeks.

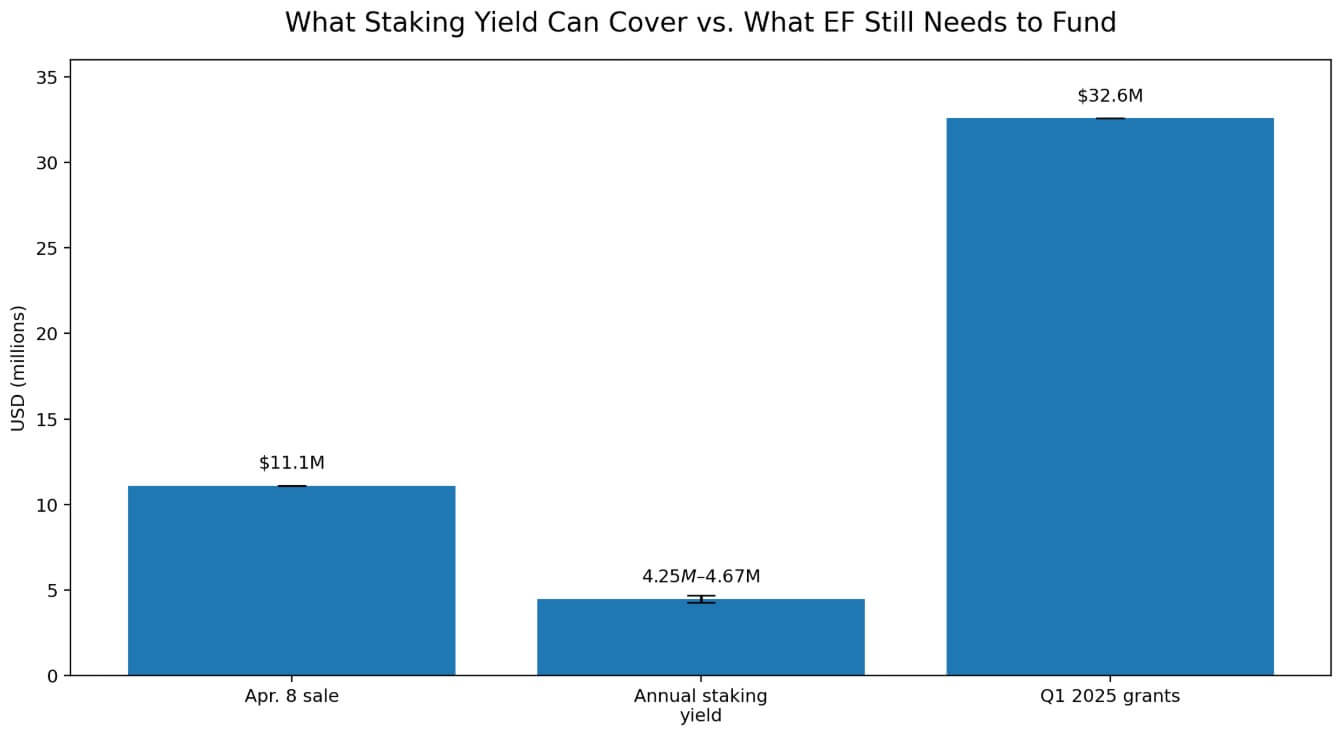

At an ETH worth of roughly $2,220.76, 5,000 ETH equal to roughly $11.1 million, the ETH staking customary charge firstly of April was hovering round 2.73% to three.00%.

70,000 ETH, producing roughly 1,912 to 2,102 ETH per 12 months, equal to roughly $4.25 million to $4.67 million at present costs. One 5,000 ETH sale corresponds to roughly 2.4-2.6x annual yield from the complete 70,000 ETH staking sleeve.

Whereas staking packages enhance treasury effectivity and cut back funding necessities, they continue to be nicely beneath the dimensions wanted to exchange treasury gross sales.

The EF’s June 2025 framework units annual working prices at 15% of the Treasury and an working buffer of two.5 years, which means fiat reserves equal to 37.5% of the Treasury.

The October 31, 2024 report, which applies solely by the use of instance to EF’s final total monetary snapshot, reveals complete treasury of $970.2 million and non-crypto property of $181.5 million, suggesting coverage goal reserves of roughly $363.8 million.

EF has already publicly added to its stablecoin publicity after that snapshot, deploying 2,400 ETH and roughly $6 million in stablecoins to Morpho in October 2025, and subsequently asserting further ETH to stablecoin conversions in October 2025 and April 2026.

The present actual measurement of EF’s fiat-like bucket and whether or not tokenized RWA holdings have already been added to the fabric measurement remains to be unknown. Subsequently, the 2024 snapshot ought to nonetheless be handled as illustrative slightly than an alternative to immediately’s stability sheet.

EF’s personal allocation replace confirmed the grant for the primary quarter of 2025 at $32.6 million. At immediately’s ETH worth, that is equal to roughly 14,700 ETH. The April 8 diversion covers solely about 33% of complete grants for the quarter, excluding protocol analysis, staffing, operations and broader trade help.

Yields and borrowings go away you with a fiat-denominated funds, however it nonetheless requires common monetization.

potential penalties

The bullish case for EF relies on easy arithmetic from Treasury, as rising ETH costs and decrease long-term funding ratios enable the inspiration to keep up greenback buffers whereas monetizing fewer cash.

| state of affairs | what is going to change | In all probability the Treasury impact |

|---|---|---|

| bull case | ETH worth rises, long-term funding ratio declines | Fewer cash have to be offered to keep up fiat buffers |

| primary case | Combined technique continues | Staking, DeFi, borrowing, and common gross sales coexist |

| bear case | ETH worth falls, spending strain will increase | Extra ETH might have to be monetized to keep up runway |

| vital which means | Reserve targets proceed to be denominated in fiat currencies | When ETH falls, the story of “few gross sales” collapses. |

In that setting, staking rewards and selective borrowing might cut back quarterly gross sales and provides EF extra flexibility in venue choice, whether or not by means of OTC blocks, TWAP execution, or conservative DeFi positions.

Then the modernization of the Treasury will seem as a decrease cadence, a smaller clip and higher execution.

Because the EF’s reserve targets are denominated in fiat currencies, the bearish case passes by means of the identical framework in reverse.

If ETH costs fall, foundations could also be compelled to additional monetize to keep up runway, particularly in the event that they lean towards a counter-cyclical mission and spend extra aggressively in more durable market situations.

On this setup, a big staking sleeve will nonetheless generate yield, however reserve necessities might rise quicker than offsetting that yield.

Public expectations constructed round “much less promoting” would conflict with the stability sheet self-discipline that the EF had already factored into its coverage.

With the conversion of April 8, the self-discipline was introduced again into view. EF’s monetary technique already mixed DeFi deployment, stablecoin borrowing, staking, and common ETH gross sales.

The market story prolonged past written insurance policies and past the inspiration’s personal post-staking transaction data.